Connect with a Lima One expert today!

If you’d like to know more about this topic or see how it applies to your project, let’s talk.

Real Estate 101Scaling Your PortfolioUncategorized

Calculating Debt Service Coverage Ratio

As a rental property investor, how can you calculate the potential value and cash-flow of a rental property before you buy it? When you’re looking for new properties, it’s important to be able to determine which ones will be good investments for you - and which ones you should avoid. One method to determine a property’s potential value and cash-flow is to calculate the Debt Service Coverage Ratio, also known as DSCR. The DSCR represents the ratio between the monthly rental income that the property produces and the debt that you owe on the property. In this post we’ll explore how understanding DSCR will help you acquire and grow a strong rental portfolio.

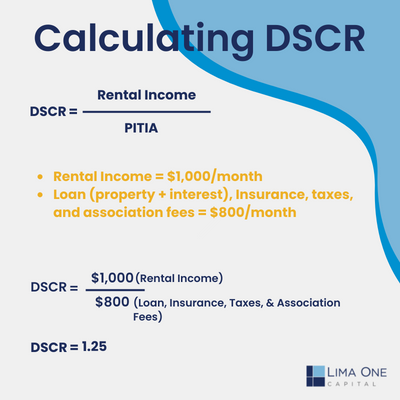

Calculating DSCR for Rental Property: How-To

To calculate DSCR, take the monthly rental income and divide it by the monthly expenses. Monthly expenses typically include the principal, interest, taxes, insurance, and - if applicable - the homeowner’s association fees that are owed on the property each month; these expenses are commonly referred to as PITIA.

For example: let's say that you buy a rental property in Atlanta, GA, expecting to be able to charge $1,500/month for rent, with the PITIA on the property coming out to be $1,000/month. Here you would divide the monthly rental income by the PITIA expenses to get a DSCR of 1.5. Since this value represents a solid return, you can expect to see a steady cash-flow from the property as long as it remains tenanted. A good rule of thumb is to keep the DSCR over 1.3 to keep your margins from being too thin, and the overall quality of the investment high. The closer you are to breaking even, the less cash-flow you’ll obtain from the property - thus making it a riskier investment.

The Importance of Calculating DSCR for Rental Property

Calculating DSCR can help you see the overall return on a property based on your estimated monthly income against your monthly expenses. Properties with a low DSCR will cost you money in the long run. By being able to calculate DSCR, you can better judge the value of a property and make smart decisions when it’s time to purchase a new property.

At Lima One Capital we are the nation’s premier lender for real estate investors. We make it easy to finance all of your fix-and-flip projects, rental properties, and multifamily investments. We are a national lender lending across the country in 46 states including Washington, D.C. We have a passion for working with real estate investors and seeing them be successful as they pursue their entrepreneurial goals. Learn more about our Rental programs and how they can help you grow your rental property portfolio. For any additional questions about rental loan program or additional loan products, feel free to contact us.

Editors note: This post was originally published in 2018 and has been updated as of August 2024 for comprehensiveness.

Subscribe for More Insights

Get the latest industry news & Lima One updates.